Starting your own business can be a daunting experience. You end up learning many new skills ranging from marketing to taxation. This may also be the first time that you don’t have a stable source of income coming into your home, which can be stressful.

However, there is a way to reduce your stress. By creating a planned objective for your new business, you can work out how much you need to live the life you want. This is your ‘lifestyle cost’.

Here’s how to calculate this figure, what you can do to reduce it, and why it is practical to make this calculation.

Take your bank statement from the past three months (you can download an Excel file from your online banking) and split your payments into the following pots:

You can add in more pots if you feel that is relevant, i.e. a childcare pot. There are no set rules for this, it is just rough guidance to get you started.

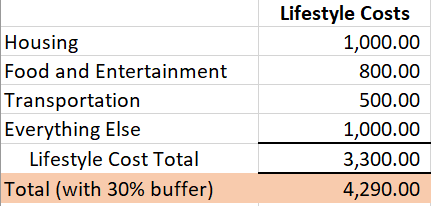

To work out the average, divide your total lifestyle cost by three (or however many months you have analysed). You should have something that looks like this:

You should include a buffer in your figure. This is for emergencies, and additional savings that you could create for you and your family. A good percentage to use is between 25% to 40% but will depend on your personal situation. We have used 30% as an illustration.

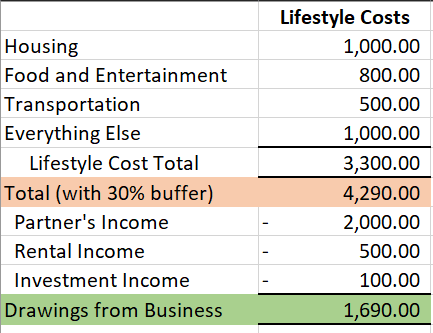

Next, you need to include any other income your household earns. Examples of this include your partner's salary, a rental or investment income.

We then deduct this from your ‘total lifestyle costs’ to determine how much you need to withdraw from your business every month.

In the example above, you would need to withdraw £1,690 from the business each month to meet your lifestyle requirements. Other income helps contribute to the overall lifestyle costs, so that you could take out less from your business.

In our example, the business may afford you to take £1,690 out from the business each month. However if it does not, you could look at reducing your expenditure.

This could mean switching to a cheaper utility provider; going on date nights at restaurants once a month rather than once a week; or even walking or cycling rather than driving. The idea is to reduce your outgoings without overly reducing your lifestyle. Small monthly savings will add up over the year.

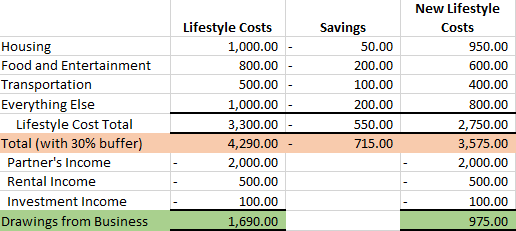

Here is an example of how big an effect some small savings can have. By reducing your spending by £550 a month, the amount you need to take from the business is now £975. Reducing the amount you take from the business allows you to invest more back into the business. It helps you grow it to where you want it to be.

This exercise also allows you to work out when you will personally run out of cash. In the above example, you would need to withdraw £975 from the business to meet your lifestyle needs, but what if you have £5,000 in your savings? If you take out £5,000 and divide by the amount you need to live on from the business, £975, we can see that you have enough savings to last five months. So instead of you withdrawing £975 from the business in the first three months say, you can spend these funds on marketing or building a good website, where the use of the spend should allow the business to reach and land more clients.

At Anderson & Edwards, we ask all of our self-employed clients to make this calculation. The reason is simple. It allows us to plan for the future and help our clients draw these funds from their business without harming it. It is also a great exercise to see where you are spending your money and whether or not you could reasonably reduce your outgoings.

Although this blog may benefit self-employed people more, it is still worth employees going through the same exercise. Should the worst happen, and you lose your job, you could then work out how much time you have to find a new job before your finances are at risk. It may even be a great time to consider launching your own business!

Every business is different, and what each business owner wants will vary. But you don’t need to do this alone. By working with an accountant, you can think about how to improve your cashflow and lifestyle costs.

Let us know if you need a hand, we help self-employed business owners like you every day. Email us at Enable JavaScript to view protected content. or phone us on 0131 364 4191.

© 2024 Anderson & Edwards Ltd|Registered in Scotland SC678768|Privacy Policy|Website by Broxden